Al iniciar este nuevo año, hemos estado recibiendo muchas consultas sobre nuestras perspectivas para el 2024. Hemos estado analizando el mercado y nos complace compartir nuestra perspectiva positiva basada en varios factores clave:

1.- Un rendimiento resiliente en 2023 que muestra una perspectiva positiva a pesar de la disminución de transacciones. A pesar de una disminución del 23.7% en las transacciones cerradas anuales en comparación con 2022, el 2023 ha demostrado ser un año sólido para el mercado inmobiliario en Marbella. Esta disminución, aunque significativa, debe ser vista en contexto, ya que sitúa al 2023 por encima del promedio de las últimas dos décadas.2014 ha experimentado una aceleración más pronunciada desde 2022 en Marbella y un ascenso sostenido en Benahavís.

2.- Los precios en Marbella y Benahavís muestran signos de moderación. En nuestro boletín reciente, resaltamos que los precios de cierre de viviendas de segunda mano están experimentando un aumento más contenido, según los datos oficiales del tercer trimestre de 2023. La información actual del portal inmobiliario Idealista de enero de 2024 sobre los precios de oferta revela una tendencia a la baja en municipios más pequeños, mientras que las ubicaciones de primera categoría mantienen la estabilidad (consulte la información adjunta para Benahavís). Esta moderación en los precios es un desarrollo positivo que podría atraer a más compradores de vuelta al mercado.

3.- La disminución del Euríbor desbloquea la asequibilidad y señala una actitud positiva en el mercado. La tasa de índice hipotecario Euríbor está en una trayectoria descendente, situándose en un 3.686% en enero de 2024 en comparación con el pico del 4.16% en octubre de 2023. Esto no solo mejora la asequibilidad para los compradores, sino que también indica un cambio favorable en el índice, anticipando reducciones adicionales, según lo pronostican diversos analistas bancarios, a lo largo de 2024 y 2025, brindando una ventana de dos años con mayor capacidad de adquisición.

4.- Las reducciones anticipadas en las tasas de interés pueden impulsar el mercado inmobiliario en 2024. Los analistas prevén una disminución de la tasa de interés oficial del Banco Central Europeo en junio, marcando otra señal positiva para el mercado. La tasa de inflación más moderada del 2.8% en enero de 2024, en comparación con las cifras de dos dígitos a fines de 2022, respalda este pronóstico. Tasas de interés más bajas aliviarán los costos hipotecarios e impactarán positivamente en el mercado inmobiliario.

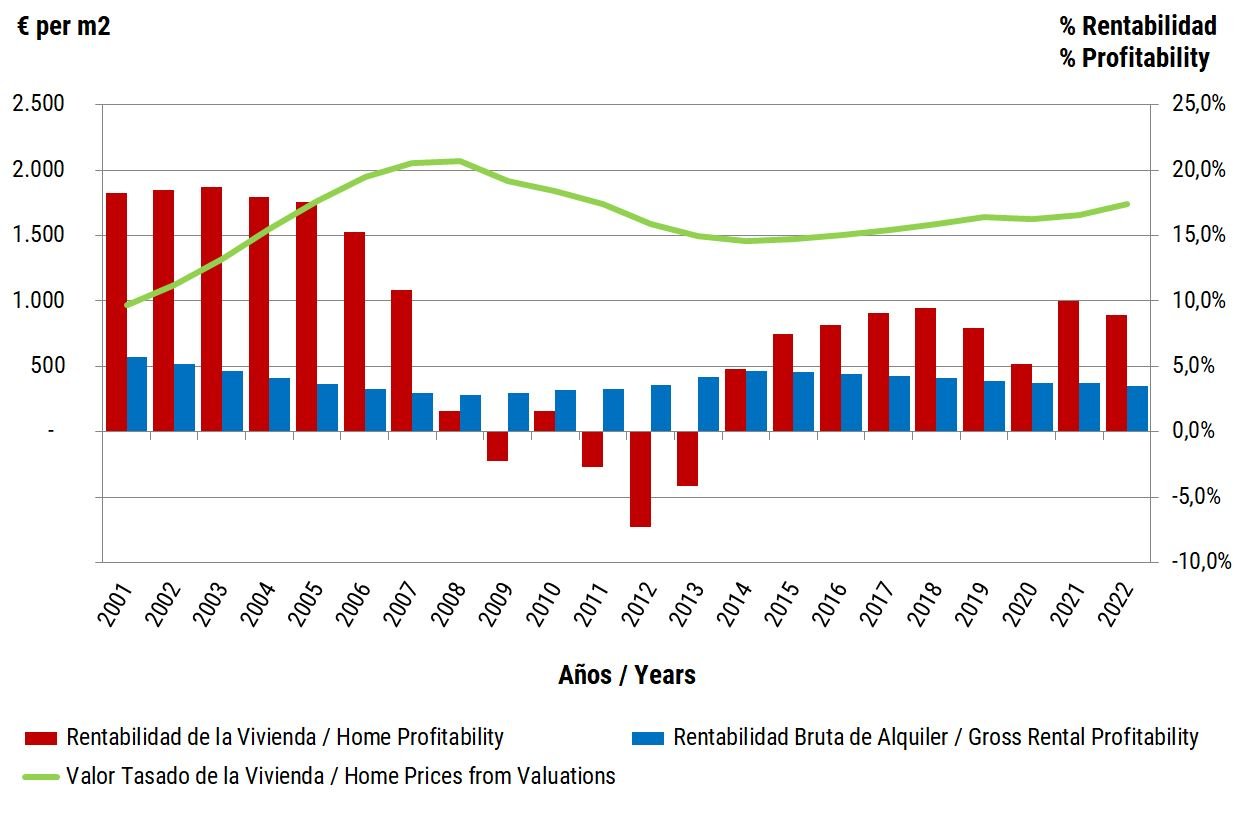

5.- Las métricas de asequibilidad están resistiendo desafíos en el panorama inmobiliario español. A pesar de un aumento del 2.25% en la tasa de asequibilidad en España en los últimos dos años, se mantiene en un 33%, aún un 1% por debajo del promedio de las últimas dos décadas. Aunque los aumentos de precios y tasas de interés han tenido cierto impacto, no se anticipa que afecten significativamente al mercado, especialmente al segmento de lujo en la Costa del Sol.

6.- El inventario constante mantiene el equilibrio en Marbella y Benahavís. El inventario permanece equilibrado y relativamente bajo. Aunque los aumentos de precios pueden alejar a algunos compradores, la oferta limitada de propiedades probablemente evitará declives significativos de precios, contribuyendo a un mercado estable.

En resumen, nuestro optimismo para el mercado inmobiliario de Marbella y Benahavís en 2024 se basa en estos indicadores positivos. A pesar de las incertidumbres geopolíticas, incluidos conflictos en Ucrania y Gaza y elecciones en Estados Unidos, creemos que el mercado, respaldado por los factores mencionados anteriormente, mostrará resistencia. Especialmente, nuestras actividades de enero han mostrado un compromiso moderado, desafiando la tranquilidad típica asociada con esta época del año.